Wow! I'm pretty amazed at how things have been going. I am trying very hard to remain skeptical, but my overall gain is pretty exciting.

I started my next round of buying today. It actually should

have been last month, but something kept me from it then. So today I bought my next round of MFI picks. Probably Monday will be my next round of Motley Fool picks. Before discussing what's new, here's a rundown of my portfolios to date.

MFI is kicking butt. 4 of 10 stocks are up dramatically, while 3 are down, one a lot (ASPV, nearly 20%). VPHM is flying, with DECK, ASEI and WNR trailing. VPHM discussed prospects at two health science conferences a couple of weeks ago, and the shares just kept going up over the course of those couple of days. ASEI has also been doing great lately - i was up more than $4 the other day, although it gave back ~$1.50 the next day. Really, this doesn't seem to be on any specific news - maybe Mr. Market is starting to value ASEI more appropriately? Also, notice that MFI is trouncing the indices. Finally, my IRR for my MFI portfolio is 59%, based on 5 months of data. Too short to conclude anything, but a nice start nonetheless.

The Motley Fool portfolio is also doing very nicely. This porfolio seems a little more

consistent: only 2 of 10 are down, and one of those is OYO the yo-yo. The rest are all up to various extents - it's still a large range, but even the least of them is significant - NATH at 8%. The IRR of my HG portfolio is 62.6%

There's my special situations portfolio. I haven't been discussing this much, because it has until recently been only one stock. I held on to LPMA after the merger, so now it's PAY. This stock has been doing nothing but rising since the merger closed - it is up ~20% since the deal closed Nov 1. I got very nervous when PAY stalled at around $32-33, and again when the earnings announcement approached. Now they're in the clear, earnings were good, and the announcement seems fine for the coming year. By a convenient coincidence, I'm reading The Warren Buffett Way by Robert Hagstrom. In it, he quotes Buffett as saying (and I'm paraphrasing) that if you know what the company is worth, then you decide the price; if you don't then the market decides the price. As nervous as I was about what to do with PAY, I realized that I don't have a sufficiently good understanding of the underlying fundamentals to decide whether Mr. Market is crazy and overvaluing or undervaluing PAY. What I'm still trying to figure out is, what do you do if the market is overvaluing the company? Sell and possibly miss out on more upside? Wait for a downturn and sell? Or sell part of the position? I've lately been listening to Jim Cramer's radio show (as a podcast), and his quote is, "Bulls make money, bears make money, but hogs get slaughtered." I wonder whether he'd tell me to take some off the table. PAY is currently the largest single position in my portfolio.

Lately, I've also become interested in TARR. It's in the dreaded housing industry. The PE is low (it was quite a bit lower when I first found the company in a stock screen), it trades near book value and it's got a high return on assets. Also, there have been a bunch of insider purchases, many of which were at prices well above where it trades now, and by several insiders. Last but not least, they are considering spinning off their homebuilding division by mid 2007. That was the icing on the cake. I do worry a little about how highly leveraged they are, but from what I've been hearing and reading, it sounds as though the housing industry is either near the bottom or possibly even just starting to turn around. If this is true, the TARR might be a great play, with a lot of potential upside. My total return on my special situations portfolio is 21%. I won't even mention the ridiculous IRR, because there's too little data in terms of total time (100 days) and total positions (2).

Finally, there's my biotech portfolio. It's full of surprises and disappointments. CBST continues to disappoint. It gapped down today, on a downgrade by Piper Jaffray. I'm not sure how much longer I will think that the market is wrong and maintain a large position in CBST. I do think that I'm right, and that it will turn a nice profit as cubicin starts to displace vancomycin (from VPHM). If I were really confident, I suppose I'd buy more, not consider selling. This is another position that requires that I do more research. CBST also announced that they'd partnered with AstraZeneca to distribute cubicin in China. It would have been nice had

they thought they could bring the drug to that market, but the royalties will be alright. Both ARNA and ALNY have risen - ARNA dropped back down, but ALNY is just going higher and higher. What's interesting about the ALNY and ARNA stories is what's similar about them: they both announced that they'd sell shares. Why? The officers must believe that the shares are overvalued. The market ignored the ALNY announcement, but ARNA plummeted (still up overall, but down dramatically from their high). Now ARNA announced the sell price, and for some reason, the stock went to well above that price. Strange - I would have thought that would have set the price, rather than selling the

bottom for the price. Anyway, the fact of the companies selling shares has made me wonder whether to sell as well. Or at least to take some off the table. ALNY especially has just kicked butt, mainly, I thought, because of the RNAI purchase and speculation that ALNY is also a buyout target. Not sure what I'll do for now.

As an aside to the discussion of my biotech portfolio, I have major seller's regret over MEDX. They have been going up like crazy over the last couple of weeks, and now yesterday one of their drugs was fast-tracked by the FDA. I'm considering getting back in MEDX, but in a several purchases at a time, so that I benefit if it goes down at all (another Cramerism).

This turned out to be a long post, so I'll discuss my new MFI purchases in a separate entry.

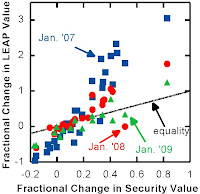

stock, I recorded the close price, as well as the close price of Jan. '07, '08 and '09 LEAPs with a strike price just below the close price of the security. Now, 4 months later, using the close as of December 8, I have determined the change in security and derivative values. LEAP values that expire in Jan. '08 and '09 changed in close accordance with stock price. (Click on the figure, and all figures, to expand them.) As the Jan. '07 expiry date approached, the LEAPs changed in price, in many cases dramatically. Of the 32 stocks that had options expiring in Jan. '07, the mean ± SD was 0.51 ± 1.05. This is a huge gain in that period of time, but much greater variability. The median change in value was 12%.

stock, I recorded the close price, as well as the close price of Jan. '07, '08 and '09 LEAPs with a strike price just below the close price of the security. Now, 4 months later, using the close as of December 8, I have determined the change in security and derivative values. LEAP values that expire in Jan. '08 and '09 changed in close accordance with stock price. (Click on the figure, and all figures, to expand them.) As the Jan. '07 expiry date approached, the LEAPs changed in price, in many cases dramatically. Of the 32 stocks that had options expiring in Jan. '07, the mean ± SD was 0.51 ± 1.05. This is a huge gain in that period of time, but much greater variability. The median change in value was 12%.

{kind=link}

{kind=link}