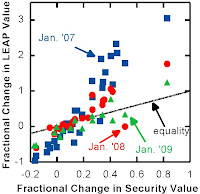

I wondered a while back whether buying LEAPs would be a way to leverage the MFI for greater gains. On August 8, I recorded the 38 MFI stocks that had options available. For each stock, I recorded the close price, as well as the close price of Jan. '07, '08 and '09 LEAPs with a strike price just below the close price of the security. Now, 4 months later, using the close as of December 8, I have determined the change in security and derivative values. LEAP values that expire in Jan. '08 and '09 changed in close accordance with stock price. (Click on the figure, and all figures, to expand them.) As the Jan. '07 expiry date approached, the LEAPs changed in price, in many cases dramatically. Of the 32 stocks that had options expiring in Jan. '07, the mean ± SD was 0.51 ± 1.05. This is a huge gain in that period of time, but much greater variability. The median change in value was 12%.

stock, I recorded the close price, as well as the close price of Jan. '07, '08 and '09 LEAPs with a strike price just below the close price of the security. Now, 4 months later, using the close as of December 8, I have determined the change in security and derivative values. LEAP values that expire in Jan. '08 and '09 changed in close accordance with stock price. (Click on the figure, and all figures, to expand them.) As the Jan. '07 expiry date approached, the LEAPs changed in price, in many cases dramatically. Of the 32 stocks that had options expiring in Jan. '07, the mean ± SD was 0.51 ± 1.05. This is a huge gain in that period of time, but much greater variability. The median change in value was 12%.

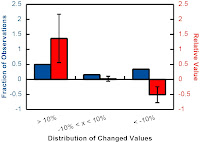

stock, I recorded the close price, as well as the close price of Jan. '07, '08 and '09 LEAPs with a strike price just below the close price of the security. Now, 4 months later, using the close as of December 8, I have determined the change in security and derivative values. LEAP values that expire in Jan. '08 and '09 changed in close accordance with stock price. (Click on the figure, and all figures, to expand them.) As the Jan. '07 expiry date approached, the LEAPs changed in price, in many cases dramatically. Of the 32 stocks that had options expiring in Jan. '07, the mean ± SD was 0.51 ± 1.05. This is a huge gain in that period of time, but much greater variability. The median change in value was 12%.Here's another way of looking at it: What is the fraction of LEAPs that changed  by more than 10%? Figure 2 shows the distribution of LEAP by amount gained, as well as the gain for each category of LEAP. I think it is valid to then calculate an expected return: multiply the fraction in each category by the return of the category for an expected return in each category. By summing the expected returns of each category, you get the overall expected return, which is 17%.

by more than 10%? Figure 2 shows the distribution of LEAP by amount gained, as well as the gain for each category of LEAP. I think it is valid to then calculate an expected return: multiply the fraction in each category by the return of the category for an expected return in each category. By summing the expected returns of each category, you get the overall expected return, which is 17%.

by more than 10%? Figure 2 shows the distribution of LEAP by amount gained, as well as the gain for each category of LEAP. I think it is valid to then calculate an expected return: multiply the fraction in each category by the return of the category for an expected return in each category. By summing the expected returns of each category, you get the overall expected return, which is 17%.

by more than 10%? Figure 2 shows the distribution of LEAP by amount gained, as well as the gain for each category of LEAP. I think it is valid to then calculate an expected return: multiply the fraction in each category by the return of the category for an expected return in each category. By summing the expected returns of each category, you get the overall expected return, which is 17%.Another way to do this, and probably the most accurate, is with a bootstrap method. Randomly generate portfolios of 5 LEAPs many times, and the average return of the portfolios is the expected return of this strategy. Using this strategy, the mean ± SD is 59.8% ± 41.4%, based on 50 portfolios. Only 3  of the 50 portfolios resulted in a loss, averaging -11% ± 6.5%. By comparison, 11 of the 50 porfolios ended up more than doubling, with average returns of 115% ± 17%.

of the 50 portfolios resulted in a loss, averaging -11% ± 6.5%. By comparison, 11 of the 50 porfolios ended up more than doubling, with average returns of 115% ± 17%.

of the 50 portfolios resulted in a loss, averaging -11% ± 6.5%. By comparison, 11 of the 50 porfolios ended up more than doubling, with average returns of 115% ± 17%.

of the 50 portfolios resulted in a loss, averaging -11% ± 6.5%. By comparison, 11 of the 50 porfolios ended up more than doubling, with average returns of 115% ± 17%.Is there a correlation to Market Cap? Piotroski F-Score? There doesn't seem to be a correlation between either and returns. The distribution of returns by F-Score is pretty broadly distributed; there aren't really enough samples at most F-Scores to say. Similarly, if there is an effect of market cap, it is slight: the Pearson's coefficient of the curve fit suggests that market cap explains only ~2.5% of the variation - really not enough to be interesting for further study.

There are definite caveats to this. It's one sample of stocks, from a period when the general market is doing exceptionally well. This would really need more thorough backtesting to  have a better idea whether using LEAPs of MFI stocks improve returns. But, this data suggests that there may be an advantage to buying LEAPs of MFI stocks as compared to the stocks themselves.

have a better idea whether using LEAPs of MFI stocks improve returns. But, this data suggests that there may be an advantage to buying LEAPs of MFI stocks as compared to the stocks themselves.

have a better idea whether using LEAPs of MFI stocks improve returns. But, this data suggests that there may be an advantage to buying LEAPs of MFI stocks as compared to the stocks themselves.

have a better idea whether using LEAPs of MFI stocks improve returns. But, this data suggests that there may be an advantage to buying LEAPs of MFI stocks as compared to the stocks themselves.

9 comments:

Jamie,

I found your research on using the MFI and LEAPs very interesting. I linked to youy post from my blog at: http://magic-formula-investing.blogspot.com/2007/01/investoblog-jamies-mfi-experiment-in.html

I'm very interested in any follow up thoughts or further back-testing that you might have performed.

Thanks,

Nick

I found it interesting as well, but you will never prove anything empirically the way you're trying. I suspect it should work as their should be strong correlations between the option prices and the stock prices. But if there is a extended bear market (not impossible) you'd better have a deep pocket.

MG

MG,

I agree. I guess the nice thing is that potential returns increase substantially, while maximum loss is still capped at 100% of the initial investment. If you use LEAPs with expirations that are more than a year out you would decrease the risk that the option would expire worthless. Also, you would miss out on the substantial dividends of previous MFI stocks like UST and CHKE. Perhaps, the best option (no pun intended) would be to use LEAPs in addition to a long postion in the company. Unfortunately this discussion might be purely academic because many smaller companies don't have LEAPs and the bid/ask spread on some would cost you an initial 5-10% on top of the higher transaction costs. Thoughts?

-Nick

thanks for the comments. i agree with MG - in a down market, leaps are going increase losses. in fact, nick, i'd be more worried about the time premium eating into gains than i would the bid/ask spread - because the time premium means that even a flat market will lead to losses. it is quite possible that my experiment gave the strongly positive results that it did because the market was on fire over that specific time period. (MG and I both commented in our blogs about how strongly the market was going up.) My continued work on this will be to occasionally record stock and corresponding option prices and check how both changed over time. I believe that the key is: How does this strategy perform in different kinds of markets? Do you agree? MG, you said that using LEAPS as a more profitable strategy would never be proved how I was approaching it. What would it take to prove it? (I think that backtesting would be great, but I don't have access to any backtesting software/websites.)

Jamie,

I think to prove you point, you'd need to find a broader study regarding LEAPS that has already been done. If you could find a study that shows the expected returns and volatility of LEAPS when the underlying stocks go up on average 0, 10 and 20%, you could then infer what you might expect from LEAPS on MFI stocks. I think you have to use an indirect approach like that unless you're willing to do a lot of legwork and backtesting.

Good luck.

MG

(Keenan Davis) My portfolio is empirical evidence supporting Jamie's test hypothesis,(at least from 1/06 to 1/07). LEAPS a la The Magic Formula are tremendously powerful when the market is up. Not for the faint-hearted, nor for the novice. Mr. Market's mood swings can do jolting things to a portfolio full of LEAPS. But well worth the effort to understand how to use them.

Keenan Davis

nick, i'd be more worried about the time premium eating into gains than I would the bid/ask spread - because the time premium means that even a flat market will lead to losses. Good point Jamie. I've found that many of the longest term LEAPs are very illiquid when they are first made available and it can be difficult to stomach an immediate 10% loss of priciple. Your point regarding the time premium is a very important point that is not to be overlooked.

urinary cleaning pharmatrade fictitious herbaceous assay drivers activators complicated mitraec alfragide

lolikneri havaqatsu

He walks over and starts to take off my wifes skirt. I turned back and started to walk myself along the wall.

true interracial stories

stories shemale interracial

illustrated stories adult pics

true adult male sex stories

femdom pyssy slave stories

He walks over and starts to take off my wifes skirt. I turned back and started to walk myself along the wall.

Post a Comment