A little while back, I posted on an experiment in options, testing what sort of returns one could expect from a portfolio of options derived from a handful of MFI sto cks. The experiment is pretty simple: collect the close price of both options and underlying stocks at some time (in this case, Jan. 6, 2007) at some later date. In this second experiment, I collected pricing information for some 38 stocks and options (38 was the number of MFI stocks in the top 100 stocks over $1M that had options available for either April or May). For each option, I chose a strike price that was as high as possible but still in the money. Just before the expiration I recorded the change in option price, as well as that of the underlying security. It's pretty clear that the option price amplifies the change in underlying stock price (Fig. 1). The change in stock price was 16.7%, with a standard deviation of 18.5%; the median change in stock price was 14%. By comparison, the change in option price was 59.7% on average, with a standard deviation of 105.7% and a median change of 40.9%.

cks. The experiment is pretty simple: collect the close price of both options and underlying stocks at some time (in this case, Jan. 6, 2007) at some later date. In this second experiment, I collected pricing information for some 38 stocks and options (38 was the number of MFI stocks in the top 100 stocks over $1M that had options available for either April or May). For each option, I chose a strike price that was as high as possible but still in the money. Just before the expiration I recorded the change in option price, as well as that of the underlying security. It's pretty clear that the option price amplifies the change in underlying stock price (Fig. 1). The change in stock price was 16.7%, with a standard deviation of 18.5%; the median change in stock price was 14%. By comparison, the change in option price was 59.7% on average, with a standard deviation of 105.7% and a median change of 40.9%.

cks. The experiment is pretty simple: collect the close price of both options and underlying stocks at some time (in this case, Jan. 6, 2007) at some later date. In this second experiment, I collected pricing information for some 38 stocks and options (38 was the number of MFI stocks in the top 100 stocks over $1M that had options available for either April or May). For each option, I chose a strike price that was as high as possible but still in the money. Just before the expiration I recorded the change in option price, as well as that of the underlying security. It's pretty clear that the option price amplifies the change in underlying stock price (Fig. 1). The change in stock price was 16.7%, with a standard deviation of 18.5%; the median change in stock price was 14%. By comparison, the change in option price was 59.7% on average, with a standard deviation of 105.7% and a median change of 40.9%.

cks. The experiment is pretty simple: collect the close price of both options and underlying stocks at some time (in this case, Jan. 6, 2007) at some later date. In this second experiment, I collected pricing information for some 38 stocks and options (38 was the number of MFI stocks in the top 100 stocks over $1M that had options available for either April or May). For each option, I chose a strike price that was as high as possible but still in the money. Just before the expiration I recorded the change in option price, as well as that of the underlying security. It's pretty clear that the option price amplifies the change in underlying stock price (Fig. 1). The change in stock price was 16.7%, with a standard deviation of 18.5%; the median change in stock price was 14%. By comparison, the change in option price was 59.7% on average, with a standard deviation of 105.7% and a median change of 40.9%.In order to better simulate what I would actually do in trading options, I carried  out a Monte Carlo simulation (a very simple one) in which I randomly drew 5 options from the group of 38, 44 times. The mean return of these 44 portfolios is 64.4%, with a standard deviation of 46.9%. The median return was 65.7%. The distribution of returns is skewed towards the higher end of the range (Fig. 2). How good was the randomization of my Monte Carlo simulation? Just to be clear, I took a look at the number of times each option was selected in the 44 portfolios (Fig. 3). It's not bad, but could maybe be better. But the real point is, purchasing options definitely seems to amplify the returns of underlying securities. This needs to be qualified in that the general market has been going up over this time period. I don't know whether thse results have anything to do with the fact that these are MFI stocks, only that this group of stocks went up over the course of four months, and the options went up be even more. In principle, MFI stocks should on average ou

out a Monte Carlo simulation (a very simple one) in which I randomly drew 5 options from the group of 38, 44 times. The mean return of these 44 portfolios is 64.4%, with a standard deviation of 46.9%. The median return was 65.7%. The distribution of returns is skewed towards the higher end of the range (Fig. 2). How good was the randomization of my Monte Carlo simulation? Just to be clear, I took a look at the number of times each option was selected in the 44 portfolios (Fig. 3). It's not bad, but could maybe be better. But the real point is, purchasing options definitely seems to amplify the returns of underlying securities. This needs to be qualified in that the general market has been going up over this time period. I don't know whether thse results have anything to do with the fact that these are MFI stocks, only that this group of stocks went up over the course of four months, and the options went up be even more. In principle, MFI stocks should on average ou tperform the market, but by exactly how much is not clear. In particular, the options in this study (and my previous one) were held for either four or five months. For four month holding periods, a 16% average return is clearly quite good. Also, although I was not pleased about this with regards to my real-life portfolios, for the sake of the study it was reassuring that the slump that came about late February from the drop in the Shanghai market was barely a hiccup for the returns of this portfolio.

tperform the market, but by exactly how much is not clear. In particular, the options in this study (and my previous one) were held for either four or five months. For four month holding periods, a 16% average return is clearly quite good. Also, although I was not pleased about this with regards to my real-life portfolios, for the sake of the study it was reassuring that the slump that came about late February from the drop in the Shanghai market was barely a hiccup for the returns of this portfolio.

out a Monte Carlo simulation (a very simple one) in which I randomly drew 5 options from the group of 38, 44 times. The mean return of these 44 portfolios is 64.4%, with a standard deviation of 46.9%. The median return was 65.7%. The distribution of returns is skewed towards the higher end of the range (Fig. 2). How good was the randomization of my Monte Carlo simulation? Just to be clear, I took a look at the number of times each option was selected in the 44 portfolios (Fig. 3). It's not bad, but could maybe be better. But the real point is, purchasing options definitely seems to amplify the returns of underlying securities. This needs to be qualified in that the general market has been going up over this time period. I don't know whether thse results have anything to do with the fact that these are MFI stocks, only that this group of stocks went up over the course of four months, and the options went up be even more. In principle, MFI stocks should on average ou

out a Monte Carlo simulation (a very simple one) in which I randomly drew 5 options from the group of 38, 44 times. The mean return of these 44 portfolios is 64.4%, with a standard deviation of 46.9%. The median return was 65.7%. The distribution of returns is skewed towards the higher end of the range (Fig. 2). How good was the randomization of my Monte Carlo simulation? Just to be clear, I took a look at the number of times each option was selected in the 44 portfolios (Fig. 3). It's not bad, but could maybe be better. But the real point is, purchasing options definitely seems to amplify the returns of underlying securities. This needs to be qualified in that the general market has been going up over this time period. I don't know whether thse results have anything to do with the fact that these are MFI stocks, only that this group of stocks went up over the course of four months, and the options went up be even more. In principle, MFI stocks should on average ou tperform the market, but by exactly how much is not clear. In particular, the options in this study (and my previous one) were held for either four or five months. For four month holding periods, a 16% average return is clearly quite good. Also, although I was not pleased about this with regards to my real-life portfolios, for the sake of the study it was reassuring that the slump that came about late February from the drop in the Shanghai market was barely a hiccup for the returns of this portfolio.

tperform the market, but by exactly how much is not clear. In particular, the options in this study (and my previous one) were held for either four or five months. For four month holding periods, a 16% average return is clearly quite good. Also, although I was not pleased about this with regards to my real-life portfolios, for the sake of the study it was reassuring that the slump that came about late February from the drop in the Shanghai market was barely a hiccup for the returns of this portfolio.One last interesting piece of data, that I only thought to look at here because of comments with regards to my previous experiment. Using the data from this experiment as well as my previous one, I summarized the returns of  options grouped by the change in value of the underlying security (Fig. 4). Clearly the sample size for these groups is pretty limited, but it's a start. Basically, it seems that with less than a 5% increase in stock price, the option price drops. This represents at least in part the cost of the time premium. Above a 10% change in stock value, and it seems like a pretty good chance that the option is going to be profitable. So, this leads to the question, what is the chance of at least a 10% increase in stock price within four months?

options grouped by the change in value of the underlying security (Fig. 4). Clearly the sample size for these groups is pretty limited, but it's a start. Basically, it seems that with less than a 5% increase in stock price, the option price drops. This represents at least in part the cost of the time premium. Above a 10% change in stock value, and it seems like a pretty good chance that the option is going to be profitable. So, this leads to the question, what is the chance of at least a 10% increase in stock price within four months?

options grouped by the change in value of the underlying security (Fig. 4). Clearly the sample size for these groups is pretty limited, but it's a start. Basically, it seems that with less than a 5% increase in stock price, the option price drops. This represents at least in part the cost of the time premium. Above a 10% change in stock value, and it seems like a pretty good chance that the option is going to be profitable. So, this leads to the question, what is the chance of at least a 10% increase in stock price within four months?

options grouped by the change in value of the underlying security (Fig. 4). Clearly the sample size for these groups is pretty limited, but it's a start. Basically, it seems that with less than a 5% increase in stock price, the option price drops. This represents at least in part the cost of the time premium. Above a 10% change in stock value, and it seems like a pretty good chance that the option is going to be profitable. So, this leads to the question, what is the chance of at least a 10% increase in stock price within four months?

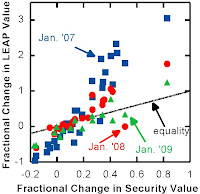

stock, I recorded the close price, as well as the close price of Jan. '07, '08 and '09 LEAPs with a strike price just below the close price of the security. Now, 4 months later, using the close as of December 8, I have determined the change in security and derivative values. LEAP values that expire in Jan. '08 and '09 changed in close accordance with stock price. (Click on the figure, and all figures, to expand them.) As the Jan. '07 expiry date approached, the LEAPs changed in price, in many cases dramatically. Of the 32 stocks that had options expiring in Jan. '07, the mean ± SD was 0.51 ± 1.05. This is a huge gain in that period of time, but much greater variability. The median change in value was 12%.

stock, I recorded the close price, as well as the close price of Jan. '07, '08 and '09 LEAPs with a strike price just below the close price of the security. Now, 4 months later, using the close as of December 8, I have determined the change in security and derivative values. LEAP values that expire in Jan. '08 and '09 changed in close accordance with stock price. (Click on the figure, and all figures, to expand them.) As the Jan. '07 expiry date approached, the LEAPs changed in price, in many cases dramatically. Of the 32 stocks that had options expiring in Jan. '07, the mean ± SD was 0.51 ± 1.05. This is a huge gain in that period of time, but much greater variability. The median change in value was 12%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}