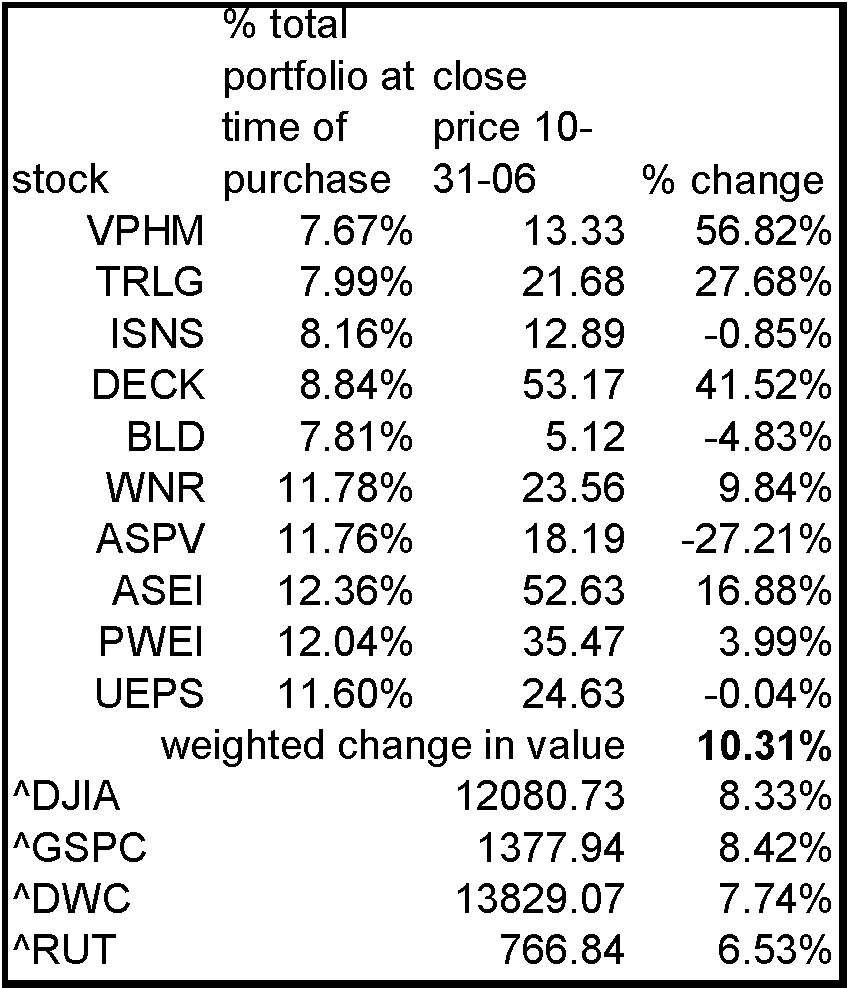

Continuing with the analysis of UEPS as recommended by Christopher Browne in The Little Book of Value Investing, now is the part that I suppose is more art and less science, at least as compared to income and balance sheet analysis.

1. Can the company raise prices?

The answer is no. The product is for people without access to banks, or people for whom bank fees are prohibitive. These are not people who can afford to pay more. The UEPS model requires more people to be part of their network, not to charge their network high fees. Having said that, though, they are positioned to find new applications for their smartcard products - both geographically (old applications in new countries) and systematically (new applications in established countries).

2. Can the company sell more?

Definitely. Their technology has been broadly adopted in South Africa, they currently operate in Namibia, Botswana and Nigeria, and are exploring opportunities in nearby African countries, as well as a number of South American and South Asian countries. Third parties are operating their technology in Malawi, Mozambique, Zimbabwe, Ghana, Rwanda, Burundi and Latvia. I would prefer that they were operating their own technology - to me this means that perhaps they couldn't keep make the most of their technology, and so resorted to licensing it out. But it's a start. In addition, they mainly operate by distribution of social welfare and payroll distribution; but they've identified additional mechanisms for adoption, including medical welfare distribution.

3. Can they increase profits on existing sales?

Not sure. Probably not, at least not any time soon. They need to expand as much as possible. Once much better established, they could probably spend less on network expansion, increasing the number of point of sales card readers, possibly once better established they can rely on government contracts to a greater extent than they do now. But for now, they need to reinvest the money they make into expansion. Revenue has gone up, but cost of goods sold has remained constant for 2005 and 2006.

4. Can the company control expenses? What is the outlook for SG&A?

SG&A went up $6M in 2005, and $3M in 2006. I showed earlier that SG&A is declining as a percentage of gross revenue, and this seems to indicate that the company is indeed controlling expenses.

5. If the company raises sales, how much goes to the bottom line?

Comparing 2006 and 2005 as an example, revenues went up a ton, cost of goods sold was constant, SG&A went up just a bit. This seems to be asking about the net profit margin, and I showed that this is increasing yearly. So historically, they've been successful with this - the question is whether they'll continue to do so, but there's no reason to think that they will not.

6. Can the company be as profitable as it used to be, or at least as profitable as its competitors?

The company is increasing profitability year-over-year. I'll compare it to competitors shortly.

7. Does the company have one-time expenses that won't need to be paid in the future?

They acquired Prism in 2006, but after the end of the fiscal year. Next year will have a $95.2M charge that is one-time. There was a similar charge in 2004, for reorganization involved in the acquisition of Aplitec.

8. Does the company have unprofitable ops they can shed?

I don't see any.

9. Is the company comfortable with Wall Street earnings estimates?

They don't seem to discuss earnings estimates in the annual report. According to

Yahoo! Finance, they seem to have come in within pennies of analyst earnings estimates in recent quarters.

10. How will the company grow in the next five years? How?

I've pretty much covered this one. It looks as though they have some pretty good prospects for growth.

11. What will the company do with excess cash?

Seems as though it will be reinvested in the company for continued growth.

12. What does the company expect its competitors to do?

They don't seem to discuss this much. They do discuss the risks of competitors, including retail banks as well as other companies that are direct competitors, but not much of what they think their strategy will be. Basically, the risks are that users will prefer special bank accounts that offer reduced charges, or that they will prefer their competitors.

13. How does the company compare financially to competitors?

I'll get into this shortly.

14. What would the company be worth if it were sold?

Hm. Interesting question. It seems that each industry has some 'typical' multiple of cash flow that is how it is valued for buyout. I'm not sure how to figure this out, but I'll play around with some numbers and come back to this.

15. Does the company plan to buy back stock?

I don't see plans to do so, but the company did buy back nearly 150,000 shares at $26.75, more than the price it's trading at now. However, this seems to have been somehow tied to purchases made by employees, maybe in a company stock puchase plan.

16. Are insiders buying?

One director bought a ton in June; A number of officers exercised options in June and one more did as well in September, all without selling their options immediately. Perhaps the options were going to expire; but I've read somewhere that exercising the options but not selling may be a sign that they are very bullish - that it somehow minimizes the tax implication for the potential gain.

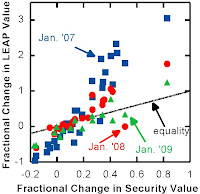

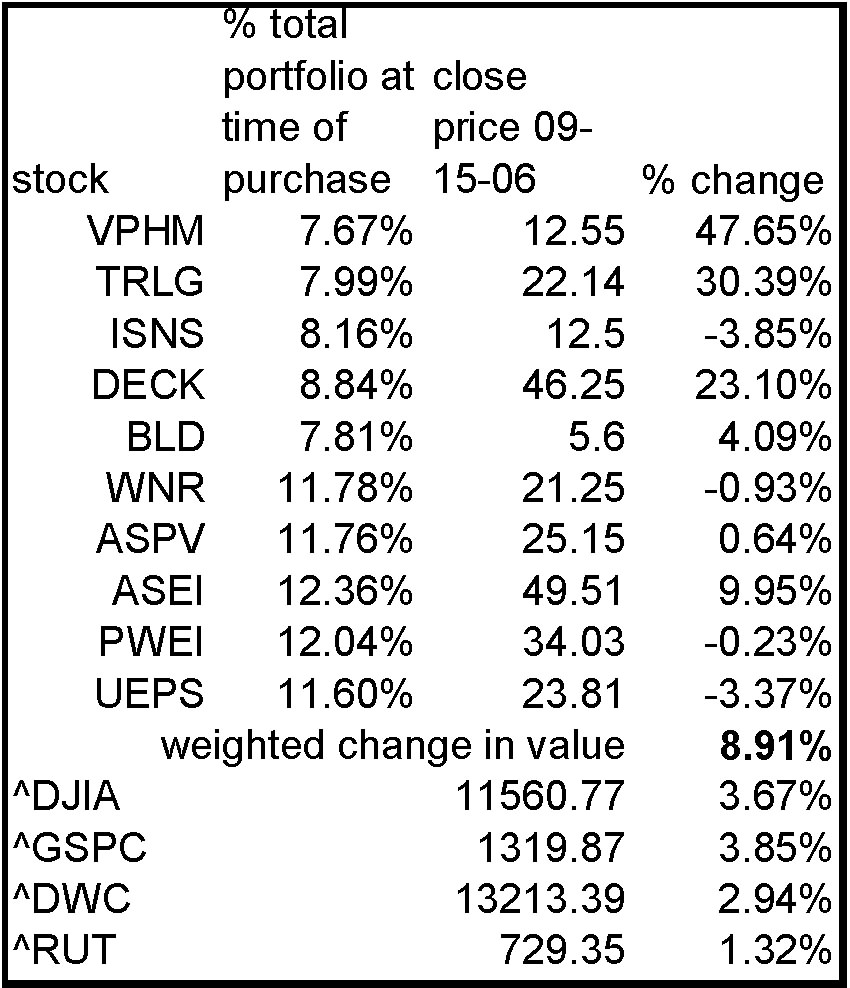

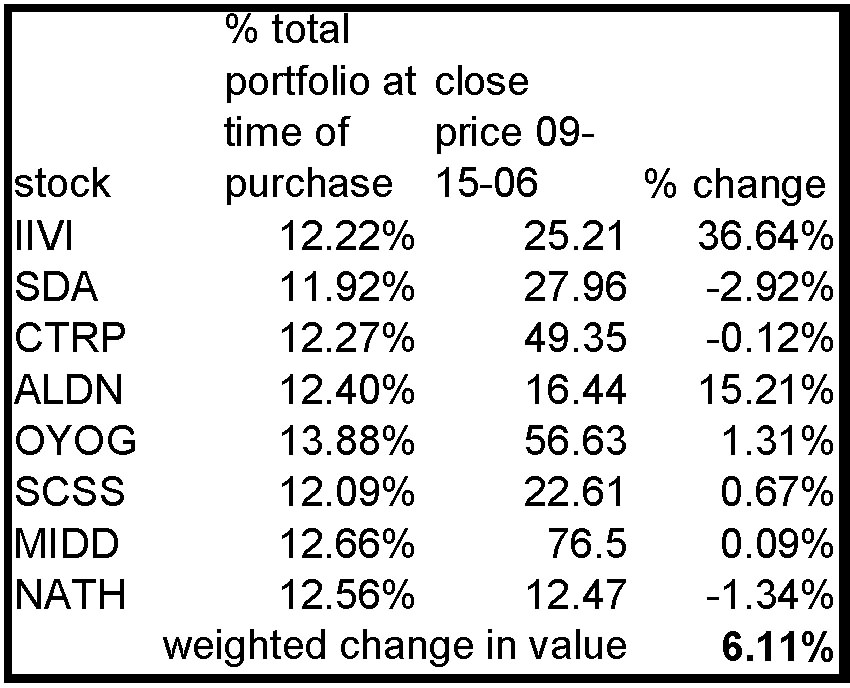

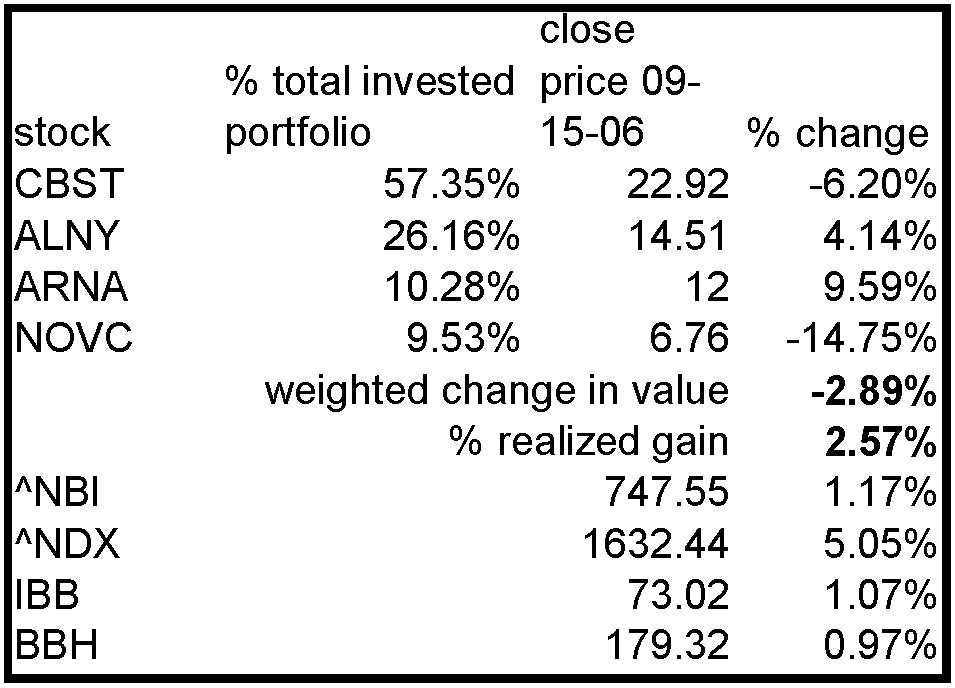

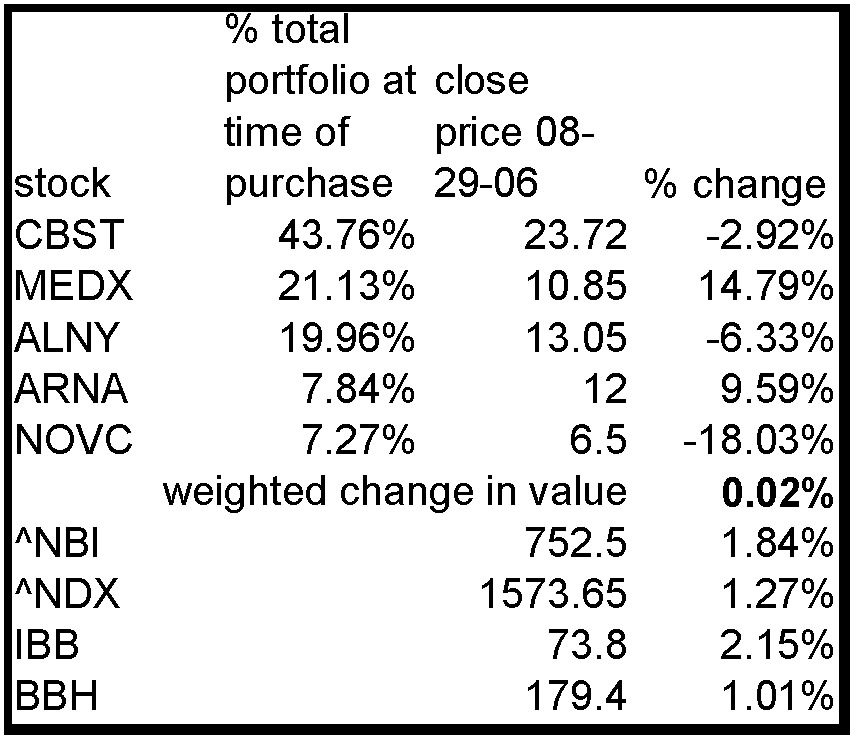

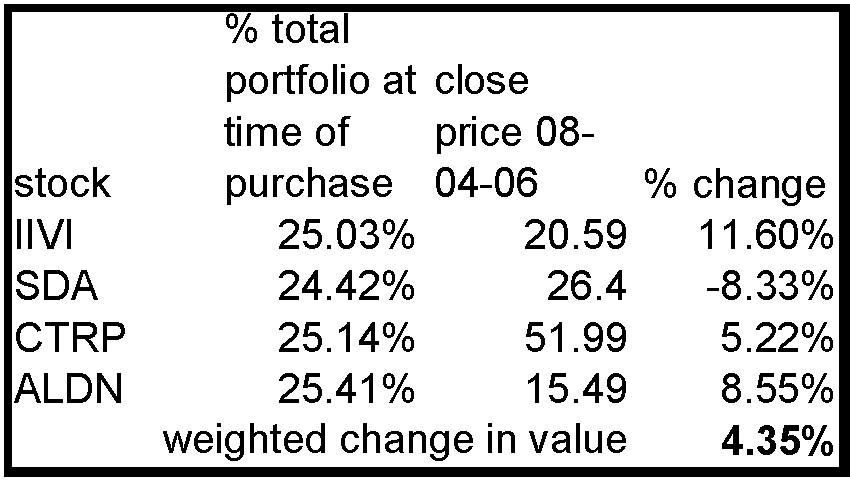

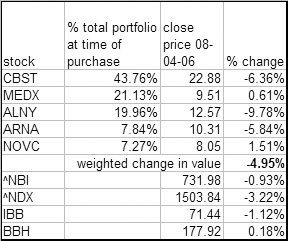

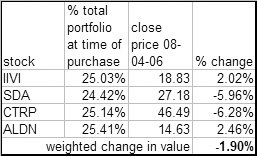

stock, I recorded the close price, as well as the close price of Jan. '07, '08 and '09 LEAPs with a strike price just below the close price of the security. Now, 4 months later, using the close as of December 8, I have determined the change in security and derivative values. LEAP values that expire in Jan. '08 and '09 changed in close accordance with stock price. (Click on the figure, and all figures, to expand them.) As the Jan. '07 expiry date approached, the LEAPs changed in price, in many cases dramatically. Of the 32 stocks that had options expiring in Jan. '07, the mean ± SD was 0.51 ± 1.05. This is a huge gain in that period of time, but much greater variability. The median change in value was 12%.

stock, I recorded the close price, as well as the close price of Jan. '07, '08 and '09 LEAPs with a strike price just below the close price of the security. Now, 4 months later, using the close as of December 8, I have determined the change in security and derivative values. LEAP values that expire in Jan. '08 and '09 changed in close accordance with stock price. (Click on the figure, and all figures, to expand them.) As the Jan. '07 expiry date approached, the LEAPs changed in price, in many cases dramatically. Of the 32 stocks that had options expiring in Jan. '07, the mean ± SD was 0.51 ± 1.05. This is a huge gain in that period of time, but much greater variability. The median change in value was 12%.

{kind=link}

{kind=link}

{kind=link}